1. Introduction

Africa’s energy sector has seen a substantial increase in investment, with capital expenditure (CapEx) reaching $47 billion in 2024, representing a 23% increase from 2023. This report provides a technical analysis of investment trends, emerging players, exploration activity, and future opportunities in Africa’s oil and gas industry.

2. Investment Trends

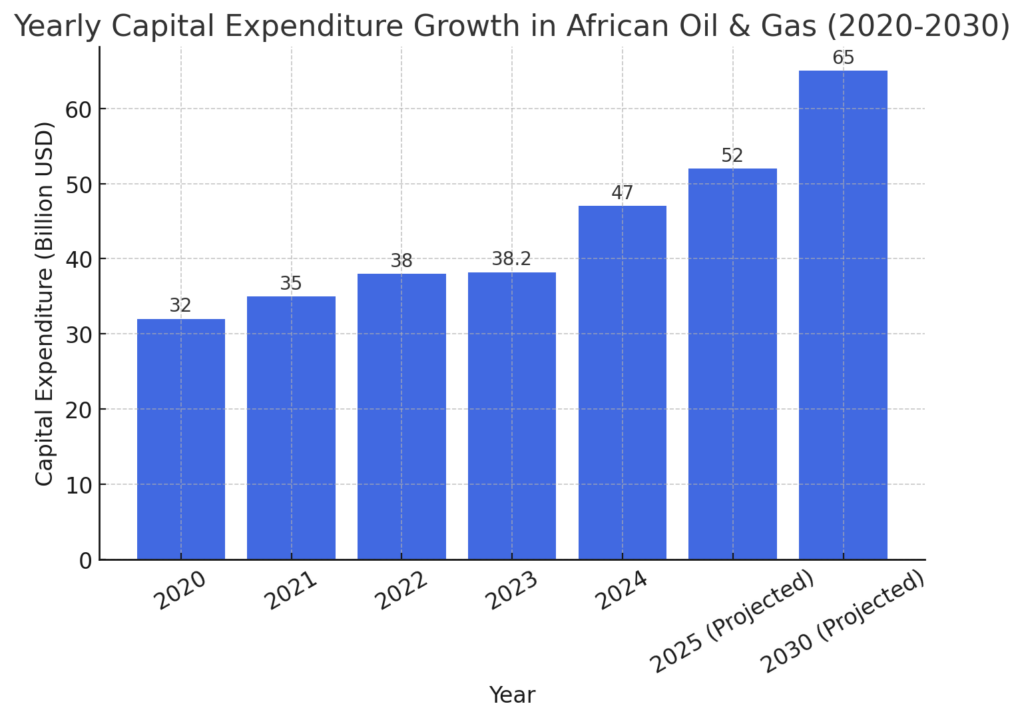

2.1 Yearly CapEx Growth in African Oil & Gas (2020-2030)

| Year | Capital Expenditure (Billion USD) | Growth Rate (%) |

|---|---|---|

| 2020 | 32 | – |

| 2021 | 35 | 9.4 |

| 2022 | 38 | 8.6 |

| 2023 | 38.2 | 0.5 |

| 2024 | 47 | 23 |

| 2025 (Projected) | 52 | 10.6 |

| 2030 (Projected) | 65 | 38.3 |

Figure 1: Historical and Projected CapEx Growth in Africa (2020-2030)

The increase in foreign investment and domestic energy policies has spurred capital injection into the sector. Emerging players such as Namibia, Senegal, and Ghana are contributing to this growth alongside established producers like Nigeria and Angola.

3. Emerging Players and Production Growth

| Country | Oil Production Growth (%) | Gas Production Growth (%) |

|---|---|---|

| Senegal | First offshore oil production | – |

| Ghana | 10% | 7% |

| Namibia | 12 new wells in 2025 | – |

| Nigeria | 5% | 8% |

Namibia, a rising exploration powerhouse, is projected to drill over 12 offshore wells in 2025 and begin production by 2029. By 2030, Namibia aims to be one of Africa’s top five producers.

4. Exploration & High-Impact Discoveries

Africa is leading in high-impact exploration wells, with 1,060 wells drilled in 2024, surpassing levels last seen in 2015.

Notable Discoveries in 2024:

- Mopane Complex (Namibia): Estimated 10 billion BOE, one of the largest offshore discoveries globally.

5. Natural Gas Reserves and Future Demand

Africa holds nearly 18 trillion cubic meters of natural gas reserves, positioning the continent as a key player in the global energy transition.

| Year | CapEx on Natural Gas (%) |

|---|---|

| 2023 | 30 |

| 2024 | 35 |

| 2025 | 38 (Projected) |

| 2030 | 40+ (Projected) |

Example: Senegal’s Greater Tortue Ahmeyim gas field will commence production in 2025, with Yakaar-Teranga awaiting a final investment decision.

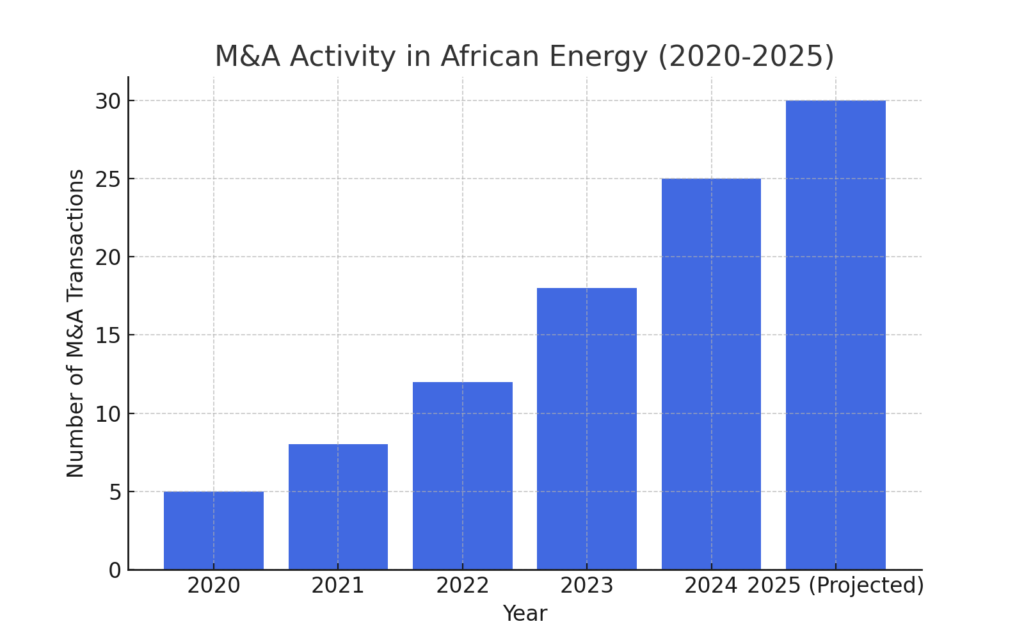

6. Mergers & Acquisitions in African Energy

The past year has seen a shift in asset ownership, with major international oil companies (IOCs) divesting mature assets. Traditionally, IOCs have held dominant positions in Africa’s energy landscape, but recent years have witnessed a strategic shift towards streamlining portfolios, focusing on low-carbon projects and high-yield new developments.

Key trends include:

Afentra acquiring Azule’s assets in Angola, aiming to increase national production.

Asian & Middle Eastern NOCs acquiring stakes in Egypt, Mozambique, Namibia, Kenya, and South Africa.

Aradel Holdings becoming Nigeria’s largest oil company after acquiring Shell’s assets.

Figure 2: M&A Activity in African Energy (2020-2025)

This trend reflects a strategic shift where major oil companies are selling mature, high-cost assets to focus on new projects and lower-carbon energy investments. At the same time, regional and independent players are seizing the opportunity to expand their footprint in the African market.

6.2 Market Dynamics and Investment Strategy

- Local and regional independents are well-positioned to enhance efficiency and extend the operational life of acquired assets.

- Governments in key markets are supporting this transition with tax incentives and regulatory adjustments to encourage domestic energy development.

- Environmental and economic benefits include optimized asset management, increased production, and reduced emissions through modernization.

This ongoing reshuffling of assets within the industry presents new avenues for investment, particularly for companies seeking to leverage Africa’s energy potential.

7. Policy Impacts on Energy Investments

Investment growth has been fueled by policy changes in Namibia, Senegal, Mauritania, Egypt, and Angola, such as:

- Tax incentives for foreign investors.

- Reduction in government profit shares to encourage regional players.

- Fast-tracking of regulatory approvals for exploration and development.

8. Conclusion

The surge in African energy investment is driven by favorable policies, new discoveries, and growing global energy demand. While international majors continue to play a dominant role, local companies are emerging as key players through acquisitions and expansions. Africa’s vast untapped resources position it as a critical energy hub for the next century.